Our partner, XM, lets you access a free demo account to apply your knowledge.

No hidden costs, no tricks.

Since crypto is not considered a currency by governments, people tend to think that crypto is not being taxed. So you might be surprised to find out that cryptos are taxable, as the IRS considers cryptos to be taxable assets. This means that your crypto assets are treated the same way as your other assets such as stocks.

The IRS requires people to fill out Form 1040 when filing for taxes, where they have to specify if they have made any transactions related to virtual currency. Big crypto exchanges are now required to file a 1099-K for clients who throughout the year have made more than 200 transactions and $20,000 in trading.

So even though governments don't consider crypto to be legal tender, the tax man still wants a slice of the pie.

“No nation has ever taxed itself into prosperity.” - Rush Limbaugh

There are many different crypto-related activities such as mining, trading, etc. But not each of these activities is taxable. Because taxes can get complicated, and we can get in big trouble if we make mistakes while filing our tax forms, we need to know exactly what activities we should count towards tax.

If you want to purchase crypto using a fiat currency you will be happy to know that this activity alone is not taxable. Also, if you purchased crypto on an exchange and transferred it to your personal wallet, you don’t have to pay taxes on it.

So if you want to purchase crypto with a plan to hold it for a very long time, you can do it knowing that you won’t have to think of paying any tax on them, as long as it just sits in your wallet without being used for anything.

This is where taxes come into play. Whenever you exchange your crypto for fiat currencies, exchange one crypto for another by using crypto exchanges, or use crypto as a payment method, you are required to list those transactions on your tax form.

Because of this, whenever you are trading crypto be very careful and record everything. The IRS started paying closer attention to crypto transactions this year and cracking down on those who dodge their crypto taxes.

NFTs are non-fungible tokens. They can be anything as long as it is digital. Art, trading cards, virtual property, and more. Because these assets are non-fungible, navigating these tax regulations can be tricky.

What makes it even more tricky is that the IRS has not released any specific tax guidelines on NFTs. But in general, these taxes on NFTs will depend on two things. Are you the creator of an NFT or a buyer and are you dealing with NFTs as a hobby or a business?

When you are creating your own NFTs, there are some activities associated with it that are taxable. For example, you are creating an NFT and have to pay 0.1 Ethereum as a gas fee for your NFT to be minted. When you purchased this Ethereum it was worth $200 and at the time of minting its price was $400. What this means is that you made a transaction with crypto and that $200 increase in your Ethereum price counts as a capital gain which is taxable.

But if this is not just a hobby for you, and you frequently mint NFTs and treat it as a business, then this money we pay as a gas price when minting the NFT can be written off as a business-related expense and won’t be taxed.

When you create this NFT and decide to sell it, whenever the transaction happens, and you receive crypto as payment, it means that you earned money and have to pay taxes for it.

When we are buying and selling NFTs, taxes that apply here are similar to the taxes that apply when we purchase assets such as art paintings. Whenever you purchase an NFT for a certain amount of crypto and then sell it at a profit, it counts as capital gains and is a taxable event. But the amount of taxes will depend on if it is a long capital gain or short. You can also count losses made while trading NFTs as capital losses.

As we mentioned before, The IRS counts gains and losses made while trading crypto as capital gains/losses. But if you have not dealt with taxes before and are confused as to what capital gains and losses are, here is a simple explanation.

For example, you purchased 1 Ethereum token when it was at $500. Then some time passed, and your Ethereum is now worth $1500. This means that you saw capital gains of $1000.

On the other hand, let's say Ethereum failed, and now it is worth just $100. This means that you made a capital loss of $400. If your capital losses exceed capital gains, you can take away some amount of money from your taxable income.

There are also two ways the IRS differentiates capital gains. These are long-term capital gains and short-term capital gains. If you bought Ethereum and kept it for over a year before you sold it, you will have to pay long-term capital gains taxes. While if you traded with that Ethereum during that year, then these transactions will be subject to short-term capital gains taxes. There are different tax rates for those two taxes, with long-term capital gains taxes having lower fees in general.

There are many different ways we can earn crypto. We can be receiving crypto as a reward for mining, receiving them as a payment for services or goods, or as winnings through different giveaways and reward programs. It does not matter how you earned it. What matters is that you earned some form of income and need to record the value of that crypto at the time of acquisition. This value should be recorded in $USD. This is the fair price value of your crypto.

This fair price value is used to then calculate your gains and losses exactly. So if crypto losses or gains value it does not matter. What you report to the IRS is the price of the crypto when you acquired it.

If you want to report crypto gains and losses on your taxes, you can do it on Form 8949. When filling out this form you will be asked to provide the following information.

One of the most important things to remember is that whenever you start dealing with cryptocurrencies you are the one who should keep track of every transaction you made in order to not get in trouble with the IRS for avoiding taxes on transactions that you forgot to track.

If you are trading crypto on one exchange and keep your assets there, then it should not be a big problem to track your gains and losses. But there is a large number of traders who move cryptos from one exchange to another. For example, those who use arbitrage trading are moving cryptos across many different exchanges and wallets. This is when things get complicated as it gets hard to keep track of your transactions, and you might forget to fill in some gains and losses you made.

From 2023 this will become easier thanks to Joe Biden issuing a new bill that requires brokers and exchanges to provide form 1099-B. This means that crypto exchanges will be required to provide information about every transaction you made to the IRS. This is just one more way that government will be able to keep an eye on everything you do. So be very careful when making transactions as the IRS will now be able to trace your every move across the blockchain.

| Tax Rates | Single | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | $0 - $41,675 | $0 - $83,350 | $0 - $55,800 |

| 15% | $41,676 - $459,750 | $83,451 - $517,200 | $55,801 - $488,500 |

| 20% | > $459,750 | > $517,200 | > $488,500 |

| Tax Rates | Single | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0 - $10,275 | $0 - $20,550 | $0 - $14,650 |

| 12% | $10,276 - $41,775 | $20,551 - $83,550 | $14,651 - $55,900 |

| 22% | $41,776 - $89,075 | $83,551 - $178,150 | $55,901 - $89,050 |

| 24% | $89,076 - $170,050 | $178,151 - $340,100 | $89,051 - $170,050 |

| 32% | $170,051 - $215,950 | $340,101 - $431,900 | $170,051 - $215,950 |

| 35% | $215,951 - $539,900 | $431,901 - $647,850 | $215,951 - $539,900 |

| 37% | > $539,900 | > $647,850 | > $539,900 |

Not paying your crypto taxes will get you in trouble the same way you would get in trouble if you didn’t pay taxes on your standard income. You might face an IRS audit, have to end up paying taxes with interest, receive penalties, or even have to face criminal charges.

If you are not a millionaire and made just a few bucks while trading with crypto it is very unlikely that the IRS will come after you, as they already have their hands full with millionaires who are avoiding taxes each and every day. There is a big difference between someone who bought crypto way back for pennies and now is trying to sell it for millions and those who made $1000 while trading, but you should still disclose everything and be ready to pay the piper.

There is no statute of limitation on fraud, but if you genuinely made a mistake the IRS has a three-year look back on errors.

"I understand the political ramifications of [!bitcoin!] and I think that the government should stay out of them and they should be perfectly legal." – Ron Paul

Another problem here is whistleblowers. If someone reports you to the IRS for not paying taxes, they get a small percentage of your fine as a reward.

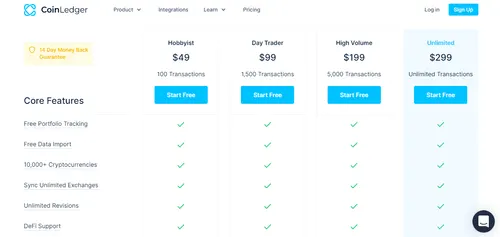

Founded in 2017, as CryptoTrader.Tax, CoinLedger is software that makes crypto tax calculations easy. This software allows users to import transaction histories from many different exchanges and then calculate capital gains they made.

One great feature that CoinLedger has is that it allows users to try out their features for free before making a decision if they want to use the product, but if you want to download your reports you need to pay.

This platform offers users four tiers of subscription. From Hobbyist to Unlimited, these tiers will track a limited number of trades, based on your subscription, with the exception being an Unlimited subscription.

CoinLedger can pretty much be connected to any exchange you use. Once you connect it to an exchange, it collects data and classifies your income as capital gains or regular income.

Then it determines what was the Fair Market Value for each transaction by converting the value of the crypto into $USD. Then it fills out a specific document form that you can use in your tax report.

CoinLedger also offers many different articles where that explain in detail how users can connect to APIs on different exchanges. Users can also integrate CryptoTrader.Tax with two other bits of tax software, namely TurboTax and TaxAct.

CoinLedger does not have many drawbacks, but one downside that it has is no free tiers. Yes, you can use a free trial of any tier but you still need to pay to be able to download the data. While there is some other crypto tax software that allows users to use their platform for free for a limited amount of trades.

Also, one inconvenience users might run into is messy integrations. Connecting CoinLedger to most exchanges is an easy process, but there are some exchanges where you might need to drop some sweat in order to do so.

"Coin Ledger is always working to improve our product to better serve our customers.. I’ve heard some critics of cryptocurrency say that tokens like Bitcoin and Ethereum are just a sophisticated way for investors to avoid taxes. Nothing could be further from the truth.. The vast majority of crypto investors are law-abiding citizens who do their best to navigate the confusing guidelines that the IRS has put in place." – David Kemmerer

Our partner, XM, lets you access a free demo account to apply your knowledge.

No hidden costs, no tricks.

No, you don’t pay taxes on crypto if you don’t trade with them. If you just purchase crypto with fiat currency and don’t complete any transactions with it, you won’t be taxed. Taxation starts when you start using that crypto.

Yes. When we are talking about cryptos and blockchain we might think that it will be hard and impossible for the IRS to track them. But most famous cryptos are not as anonymous as you might think, and the IRS has the means to track them. Also, there is new legislation that will force exchanges to send the IRS your crypto activities.

If we want to minimize the taxes on our crypto activities, we have to go for long-term gains. If we keep crypto for over a year and only after that use it to trade and make profits, it will count as long-term gain and taxes will be lower than short-term gains.

© Copyright 2022, All rights reserved